Local Real Estate Market Condition

Happy Fall! As the summer sales season winds down, I thought I’d send you some details about what’s happening here locally in the real estate market. Things are changing quickly, and uncertainty is a big part of our overall backdrop.

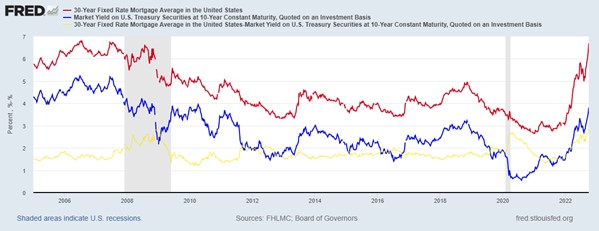

Mortgage Rates: You heard right, they hit 7% the week of September 19th ? but they retreated a bit and are hovering around 6.75%. 30-year mortgages are sold to investors as mortgage-backed securities (red line), and on average yield around 1.75% (yellow line) more than the 10-year treasury (blue line), as illustrated by this chart from the Federal Reserve.

With that in mind, the 10-year treasury is currently yielding 3.765%, assuming a 1.75% premium over the 10-year treasury, the 30-year mortgage rate should be around 5.5%. Today the 30-year mortgage at 6.8%, is yielding about 3% more than the 10-year treasury, suggesting that once certainty returns to the markets, there’s room for rates to fall.

Local Sales Activity: We’re seeing a change in purchasing and listing activity – they’re moving in step with each other, which is a good thing for existing homeowners and their home values. To keep a pulse on supply and demand, we compare the total number of homes currently listed for sale against the number of homes sold in a month to determine how many months of supply we have for sale. We’ve always considered a supply of four to six months to be balanced – using this metric, we’re still in a sellers’ market (1.3-month supply); however, that’s complicated today. We are seeing homes that are priced competitively and staged well sell quickly and, in many cases, with multiple offers. Homes that are priced incorrectly, or don’t show in their best light, are sitting on the market longer, dropping their prices, or withdrawing from the market. Year over year, the number of homes sold is down 12.3%, while the median sales price is up 8.3% and the average list price to sale price ratio is 102.2%.

Housing Affordability: When we compare the current Twin Cities median household income with a mortgage payment of a home purchased at the current median sales price, we call the resulting percentage the Housing Affordability Index. As of August 31st, this was 98. In other words, a household earning the median income could afford a home priced at 98% of the median sale price ($369,750) based on the prevailing 30-year interest rate. With rates having increased since August, I expect this index to drop lower.

What’s to come? With the chairman of the Federal Reserve recently saying the housing market will probably “have to go through a correction” on a national level, it’s hard to say how hard they’ll try to affect that and how much it will affect us locally. I do believe the “median sale price” will fall as more people start to purchase more homes in the sub-median price range (based on the affordability index), which will result in the media shouting that home prices are falling.

In 2008, mortgage qualification standards didn’t require any cash outlay from buyers nor a sufficient income to pay the monthly payment. With no skin in the game, and insufficient income to pay the monthly payment, foreclosures exploded and flooded the market with a large supply of homes (10-month supply in September 2008). With supply far exceeding demand, prices dropped.

Recently though, mortgage qualification standards require a cash down payment and wait for it: a sufficient income to pay the monthly payment. In fact, over the last two years I’ve seen more cash offers and offers with substantial down payments than I’ve ever seen before. With that said, we’re heading into this potential recession where most homeowners have a solid equity position and the ability to make the monthly payment – affording them the flexibility to hold on to their properties and wait out any Fed-induced storms.

For those that want to sell, it’s critical their house be priced and staged well to get top dollar. For the last two years that hasn’t mattered much.

For those looking to buy, I think there will be a disproportionate opportunity to build equity with houses that need a little bit of elbow grease and cosmetic work. I have several lender connections for fix-up funds if desired.

As always, if you know anyone that is interested in buying or selling, please let me know so that I can follow-up with them. I’ll be sure to strategize with them and figure out the best path forward for their specific situation.

Take Care,

Jonathan Lindstrom