There have been a lot of scary headlines lately about recessions, housing bubbles, home values dropping, etc. Google is even reporting a 200% increase in the search term “real estate housing market crash.” I happen to know a local housing expert 😉, so I thought I’d weigh in on the local housing market, what my colleagues and I are seeing right now, and what we anticipate as we head into the future as it relates to the housing market here.

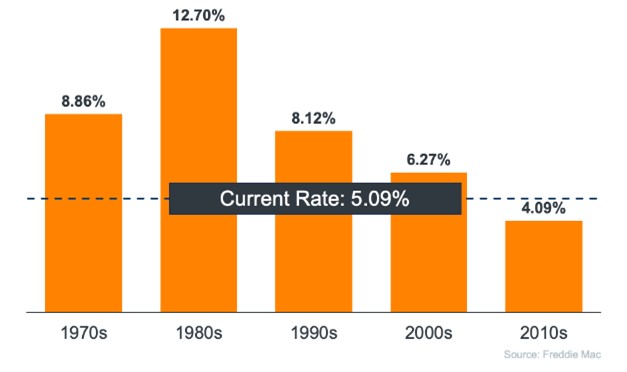

Mortgage rates are up: Rates have been volatile this year. Coming into 2022, 30-year conventional mortgage rates were around 3% – today they’re closer to 6%. That means a buyer borrowing $100,000 for 30 years in January would have paid about $422/month; that same buyer today would pay about $600/month. Most buyers purchase a home based on the monthly payment they are comfortable with, so that has decreased the buyer pool. That said, rates are still historically low (the 30-year rate is higher than what’s noted in the image).

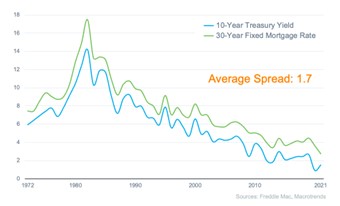

The Federal Reserve recently raised the Fed Funds Rate by 0.75%: Many people have confused that with mortgage rates – while those moves do affect mortgage rates, they’re not tied directly to them. The Fed Funds Rate is a short-term rate that banks charge each other – usually overnight. Home mortgages are usually 30-year loans, bundled together in large quantities and sold to investors as long-term investments called mortgage-backed securities. As such, they’re more closely tied to other long-term investments, like the 10-year Treasury Note. Here’s a chart illustrating that.

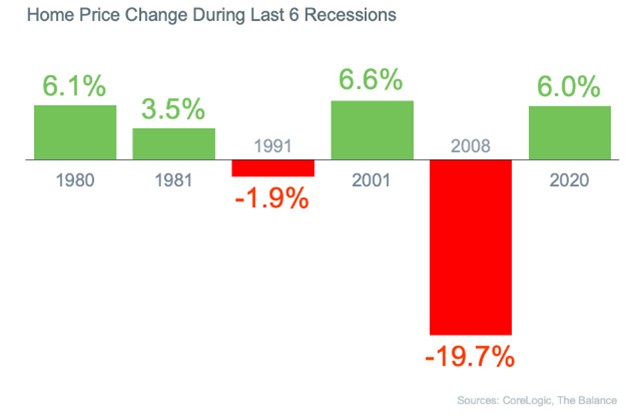

Home values probably won’t drop: For many of us, the Great Recession is still a recent memory, so it’s shaping our perception of what will happen if another recession hits. Of course, that was a housing recession fueled by terrible lending practices with many banks not verifying income or assets (“no-doc” loans). Buyers could borrow 100% of their purchase price on a variable rate loan that didn’t require them to pay the interest that accumulated each month nor reduce their principal – their mortgage balances grew every month! They bought houses they literally couldn’t afford. Now, borrowers must have a down payment, and they must prove they have sufficient income to make their payments. They’re buying houses they can afford. Did you know that home values increased in four of the last six recessions?

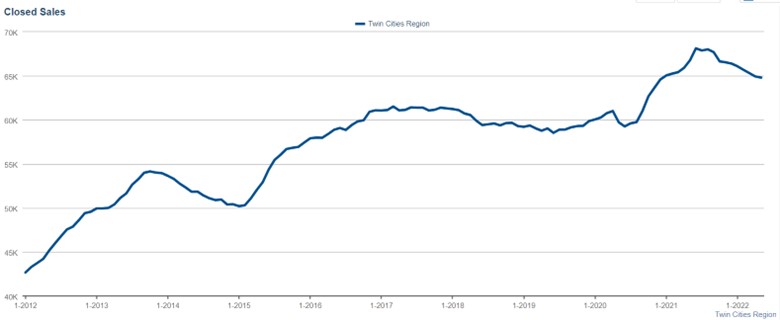

Sales are down: The number of homes sold this year has decreased from last year. BUT, last year more homes were sold than any previous year in recorded history. The number of homes sold is still higher than pre-pandemic levels:

We’re shifting towards a more balanced market: For the past two years, we’ve been in one of the strongest seller’s markets on record. We measure this by calculating how many months of housing inventory are currently for sale. If we stopped listing houses for sale today, and continued selling houses at the current rate per month, how many months would it take to run out of listings? That’s the metric. We’re currently at a 1.3-month supply, which is up from an all-time low of 0.9 months in February. A market is “balanced” when there is a four-to-six-month inventory of homes for sale. We’ve got a ways to go before we reach a balanced market, and even more to reach a buyer’s market.

Housing affordability has declined: We measure housing affordability locally based on current mortgage rates, the current median income, and the current median sales price. If a person earning the median income can afford exactly the payments on a median-priced home based on today’s mortgage rate, the Housing Affordability Index rating would be 100. Even with median sale prices rising at double digit rates, the median earner could afford more than the median-priced home until just last month. At the end of May, the median earner could afford 94% of the median priced home (currently $375,000).

The number of price drops is increasing: Don’t fall for this headline! Listing a house at any price does not make it worth that price. When home values increase as quickly as they have, sellers often want to price higher than recent sales to try and get more money. Some price high to test the market, with a plan to drop closer to market value if buyer interest is lacking.

Don’t panic! It’s hard to say what’s going to happen tomorrow, but based on what I’m seeing, I don’t see a housing crisis in our near future. I believe the increase in mortgage rates will serve to slow down the rate of home appreciation, but since our housing market is built on a solid foundation of qualified borrowers, I don’t see a repeat of 2008.

If you have any questions or would like to discuss this information further, please give me a call! And as always, if you know anyone looking to buy or sell a home, please send me their name and number so I can follow-up with them.

Take care,

Jonathan Lindstrom